What Is the Best Way to Earn Compound Interest? (Simple Guide for Beginners)

If someone asked what is the best way to earn compound interest, the short answer is: start as early as possible, choose accounts that compound frequently, and reinvest every dollar earned. But the longer answer — the one that actually changes financial outcomes — requires understanding how compound interest works, where to put money to maximize it, and critically, how it can work against someone when it comes to debt.

This guide breaks it all down: the definition, the math, the best accounts, the time factor, and the debt trap — everything needed to make compound interest a genuine wealth-building tool.

Table of Contents

ToggleWhat Is Compound Interest?

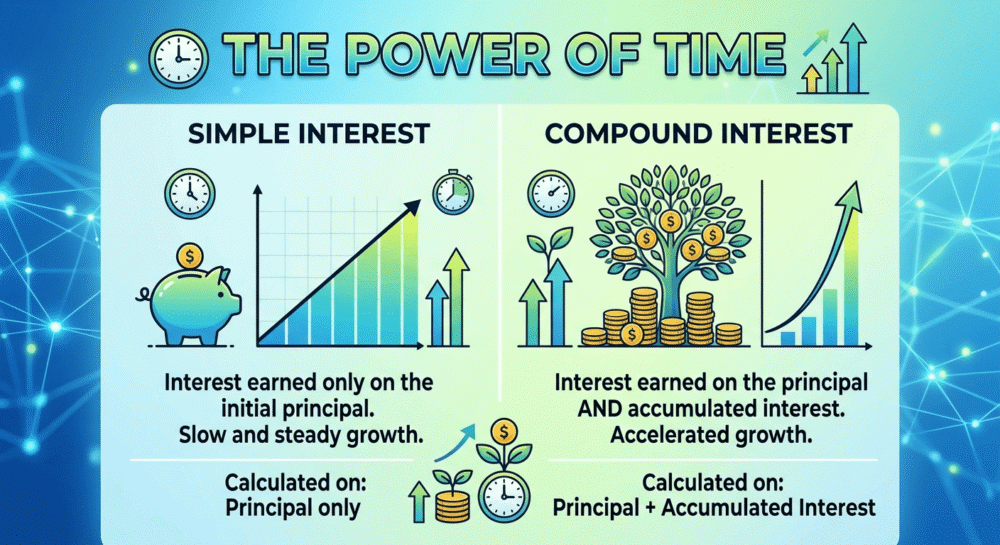

Compound interest is interest calculated on both the original principal and the accumulated interest from previous periods. Unlike simple interest, which only grows a fixed amount each period, compound interest grows exponentially — meaning money earns interest on its interest, accelerating wealth over time.

Compound Interest vs. Simple Interest

The core difference lies in what the interest is calculated on. With simple interest, the calculation is always based on the original deposit. With compound interest, every period’s earned interest gets added to the base — and then the next calculation is applied to that larger amount.

| Feature | Simple Interest | Compound Interest |

|---|---|---|

| Basis | Principal only | Principal + earned interest |

| Growth rate | Linear | Exponential |

| Best for | Short-term loans | Long-term savings/investing |

| Example (5%, 10 yrs, $1,000) | $629 earned | $500 earned |

Here is a concrete example: $1,000 at 5% simple interest for 10 years earns exactly $500 — predictable, flat, linear. The same $1,000 at 5% compound interest (compounded annually) for 10 years earns $629. The difference grows dramatically over longer timeframes.

The Compound Interest Formula Explained

The formula is: A = P(1 + r/n)^(nt). Where A = final amount, P = principal, r = annual interest rate (decimal), n = number of times interest compounds per year, t = time in years. The higher n is, the faster money grows.

To understand how each variable changes your final return in real time, you can use a compound interest calculator and experiment with different values.

This formula reveals something important: compounding frequency matters. An account compounding daily will always outperform an identical one compounding annually, even at the same stated rate.

How Does Compound Interest Work for Investing?

Understanding how compound interest works for investing is one of the most valuable financial concepts a person can learn. When someone invests in a compound-interest-bearing account or reinvests their returns, their portfolio does not grow in a straight line — it grows on a curve.

The Power of Compounding Frequency: Daily vs. Monthly vs. Annual

Compounding frequency is how often earned interest gets added to the principal. Daily compounding produces more growth than monthly, which outperforms annual. On a $10,000 deposit at 5% APR over 10 years: annual compounding yields $16,289 — daily compounding yields $16,487. The gap widens significantly over decades.

Most high-yield savings accounts compound daily and credit interest monthly, which is the best available combination for short-term savers. Investment accounts compound continuously through market returns and dividend reinvestment.

Real-World Example: $5,000 Invested Over 20 Years

Consider someone who deposits $5,000 at age 25 into an index fund averaging 8% annual returns, reinvesting all dividends:

- After 10 years: ~$10,795

- After 20 years: ~$23,305

- After 30 years: ~$50,313

- After 40 years: ~$108,623

That single $5,000 deposit becomes over $108,000 — with zero additional contributions. This is the compound interest growth example that makes wealth managers say compounding is the eighth wonder of the world.

The Rule of 72 — How to Estimate Doubling Time

The Rule of 72 is a quick mental math shortcut: divide 72 by the annual interest rate to estimate how many years it takes to double money. At 6%, money doubles in 12 years. At 9%, it doubles in 8 years. At 3% (typical savings), it takes 24 years.

Best Ways to Earn Compound Interest (Ranked)

Knowing what is the best way to earn compound interest depends on time horizon, risk tolerance, and liquidity needs. Here are the top five vehicles, ranked from lowest to highest growth potential:

1. High-Yield Savings Accounts (HYSAs)

Best for: Emergency funds, short-to-medium-term savings

HYSAs are the most accessible starting point for earning compound interest. Offered by online banks, they typically carry APYs of 4.50%–5.25% (as of 2025), far outpacing the national average savings rate of 0.45%.

- FDIC-insured up to $250,000

- Compounds daily, credits monthly

- No market risk — principal is protected

• Easily liquid — funds accessible within 1–2 business days

2. Certificates of Deposit (CDs) and CD Laddering

Best for: Savers who will not need funds for a fixed period

CDs lock in a fixed interest rate for a set term — typically 3 months to 5 years. The longer the term, the higher the rate. CD laddering — splitting deposits across multiple maturity dates — gives both higher rates and periodic access to funds.

3. Money Market Accounts

Best for: Slightly higher rates with check-writing flexibility

Money market accounts (MMAs) sit between savings accounts and checking accounts. They typically offer better rates than standard savings accounts and compound interest daily while allowing limited monthly transactions.

4. Index Funds and ETFs (Long-Term Compounding)

Best for: Long-term investors (10+ year horizon)

Index funds and ETFs deliver compound interest investing strategy at its most powerful. Returns are reinvested automatically, meaning dividends and capital gains compound year over year. The S&P 500 has delivered an average annual return of approximately 10% over the past 50 years before inflation.

- No active management required

- Low expense ratios (as low as 0.03% for some ETFs)

- Tax-advantaged options available (IRAs, 401(k)s)

5. Dividend Reinvestment Plans (DRIPs)

Best for: Investors who want to compound stock ownership over time

DRIPs allow investors to automatically reinvest dividends back into additional shares of the same stock or fund — often at no commission. Over decades, this dividend reinvestment compound interest approach can dramatically increase the number of shares held and the total return.

Why Time Is the Most Powerful Compound Interest Factor

The power of compound interest over time is unmatched by any other financial lever — including the interest rate itself. A person who starts investing early and earns a modest 6% will almost always outperform someone who starts late and earns 10%.

Starting Early vs. Starting Late — A Comparison

Investor A deposits $5,000 at age 25 at 7% annual return and adds nothing else. By age 65, they have approximately $74,872. Investor B waits until age 45 and deposits the same $5,000. By age 65, they have only $19,348. The 20-year head start is worth over $55,000 — without a single extra dollar contributed.

This is why financial advisors consistently say start investing early — not start investing big. Time is the variable that does the heavy lifting.

How to Maximize Compound Growth with Consistent Contributions

Adding regular contributions to a compound-interest account dramatically accelerates results. A monthly $100 contribution to that same 7% index fund, started at age 25:

- Age 35: ~$17,309 in contributions, ~$21,800 total

- Age 45: ~$36,000 contributed, ~$52,400 total

- Age 65: ~$84,000 contributed, ~$262,000+ total

How Does Compound Interest Work on Debt?

The same mechanism that builds wealth through investing can destroy it through debt. Understanding how compound interest works on debt is essential for anyone carrying a balance on credit cards, student loans, or personal loans.

Credit Cards: The Compounding Debt Trap

Credit card interest compounds daily on the unpaid balance. A $3,000 balance at 24% APR, with only minimum payments made, can take over 10 years to pay off and cost more than $3,000 in interest alone — more than the original purchase. This is the compounding debt trap in action.

Most credit cards use Daily Periodic Rate (DPR) — the APR divided by 365. A 24% APR card has a DPR of 0.066%. Applied daily to the balance, interest compounds relentlessly, even if no new charges are added.

Student Loans and Compounding Unpaid Interest

Federal student loans typically use simple interest during repayment. However, when interest goes unpaid — during deferment or income-driven repayment periods with low payments — it can capitalize, meaning it is added to the principal. From that point forward, the loan behaves like compound interest, charging interest on the newly inflated principal.

- Capitalized interest can add thousands to the total loan balance

- Income-driven repayment plans can cause negative amortizatio

- Paying even a small amount of interest during deferment prevents capitalization

Strategies to Reduce Compound Debt Faster

Beating the compounding debt trap requires paying more than the minimum — ideally the full balance monthly. For existing debt:

- Pay highest-interest debt first (avalanche method) to cut compounding costs fastest

- Consider balance transfer cards with 0% intro APR to buy compounding-free time

- Make bi-weekly instead of monthly payments to reduce the principal faster

- Any extra principal payment immediately reduces the base on which interest compounds

Pros and Cons of Compound Interest

Compound interest is not inherently good or bad — it is a mathematical force that amplifies whatever direction money is already moving.

When Compound Interest Works for You (Investing)

- Passive growth: Money grows without active effort

- Exponential returns: Growth accelerates over time, not just adds up

- Inflation hedge: Returns from index funds historically outpace inflation

- Accessible starting point: HYSAs and index funds require no expertise

When Compound Interest Works Against You (Debt)

- Daily compounding on debt: Credit cards compound interest every single day

- Minimum payment trap: Low payments barely cover interest, leaving principal untouched

- Loan capitalization: Unpaid interest gets added to principal, inflating future interest charges

- Psychological impact: Debt can feel impossible to escape when it grows faster than payments

Tips to Maximize Compound Interest Earnings

To truly understand what is the best way to earn compound interest, the answer comes down to four actionable habits that any saver can adopt regardless of income level:

1. Automate Contributions to Stay Consistent

Consistency is the most underrated element of earning compound interest. Setting up automatic monthly transfers to a HYSA or index fund removes decision fatigue and ensures compounding never pauses. Even in months where money feels tight, small automated contributions keep the growth engine running.

2. Choose Accounts with the Highest Compounding Frequency

When comparing savings accounts, look beyond the APY — check the compounding frequency. Accounts at the highest compounding frequency (daily) will always yield more than monthly or quarterly options at the same stated rate. Look for online banks that both compound daily and credit interest monthly.

3. Reinvest Returns Instead of Withdrawing

Every time interest or dividends are withdrawn instead of reinvested, the compounding base shrinks. Reinvesting returns is the single most important behavior that separates modest savers from serious wealth builders. In investment accounts, enable automatic dividend reinvestment (DRIP) to ensure no return goes uncompounded.

4. Minimize Debt with Compound Interest Rates

Earning 5% on savings while paying 24% on credit card debt is a losing equation. Eliminating high-interest compound debt is mathematically equivalent to earning a 24% guaranteed return — better than almost any investment available.

FAQ: Common Compound Interest Questions

What is the best way to earn compound interest with little money?

Even with $50–$100, compound interest can work meaningfully over time. Open a high-yield savings account (no minimum balance required at many online banks), or invest in a fractional share ETF through a brokerage like Fidelity or Schwab. The key is to start — the amount matters less than the time spent compounding.

How often does compound interest compound — daily, monthly, or yearly?

It depends on the account. Most high-yield savings accounts compound daily. CDs typically compound daily or monthly. Most investment accounts compound continuously through market returns. Daily compounding is the best available option for deposit accounts.

How does compound interest work on debt like credit cards?

Credit card interest is calculated daily using the Daily Periodic Rate (APR ÷ 365). If the balance is not paid in full each month, interest is charged on the outstanding balance — including previously charged interest. This is why credit card debt can spiral rapidly even without new spending.

What is the difference between compound interest and simple interest?

Simple interest is calculated only on the original principal. Compound interest is calculated on the principal plus all previously earned interest. Over long periods, the difference is enormous: $10,000 at 5% simple interest for 20 years yields $10,000 in interest. The same at 5% compound interest yields $16,533 — over 65% more.

How long does it take to double money with compound interest?

Use the Rule of 72: divide 72 by the annual interest rate to get the approximate number of years to double. At 6%, money doubles in 12 years. At 9%, it doubles in 8 years. At 1% (standard savings), it takes 72 years — which is why high-yield accounts and investing matter so much.

Conclusion: Make Compound Interest Work for You

So, what is the best way to earn compound interest? The honest answer is that there is no single account or strategy that works for everyone — but there is a universal set of principles that always holds true: start early, compound frequently, reinvest consistently, and eliminate high-interest debt as a priority.

Compound interest is one of the few financial forces that genuinely rewards patience. A person who opens a high-yield savings account today, automates monthly contributions to an index fund, and avoids carrying a credit card balance is already doing more than most people ever will.

The math does not lie. Whether it is $500 or $50,000, money placed in a compounding environment grows faster with each passing year. The longer the runway, the more dramatic the results — which means the best time to start is always right now.

Use the Rule of 72 to set realistic expectations. Check compounding frequency when comparing accounts. Revisit and reinvest returns instead of letting them sit idle. And remember: every dollar of compound debt paid off is the same as earning a guaranteed high-interest return — the compounding that was working against someone stops the moment the balance hits zero.

Compound interest does not care about income level, investment experience, or starting amount. It cares about two things: time and consistency. Give it both, and it will do the rest.